What Are the Real Risks of Buying Property in Cyprus in 2026? A Sophisticated Investor's Guide

Title deeds, Northern Cyprus, communal fees, developer default, VAT, succession. A clear-eyed look at every meaningful risk of buying property in Cyprus in 2026 — and how to mitigate each one

What Are the Real Risks of Buying Property in Cyprus in 2026? A Sophisticated Investor's Guide

Published 17 May 2026 by Kefah Abu Ghosh, Founder of Abuda

Cyprus is one of the most attractive property investment markets in Europe in 2026 — high rental yields, a favourable tax regime after the January 2026 reform, English-language transaction process, and EU-level legal infrastructure. We've written separately about why Limassol, Larnaca, and Berlin sit at the top of our investment matrix.

But the strongest return profile in the world doesn't matter if you walk into a deal blind to the risks. Cyprus has a handful of genuine, well-documented risk vectors — some are historical artefacts that have now been largely resolved, others remain live and material. Sophisticated investors don't pretend the risks don't exist; they price them, mitigate them, and walk in with eyes open.

This is a clear-eyed guide to every meaningful risk of buying property in Cyprus in 2026 — and exactly how to mitigate each one.

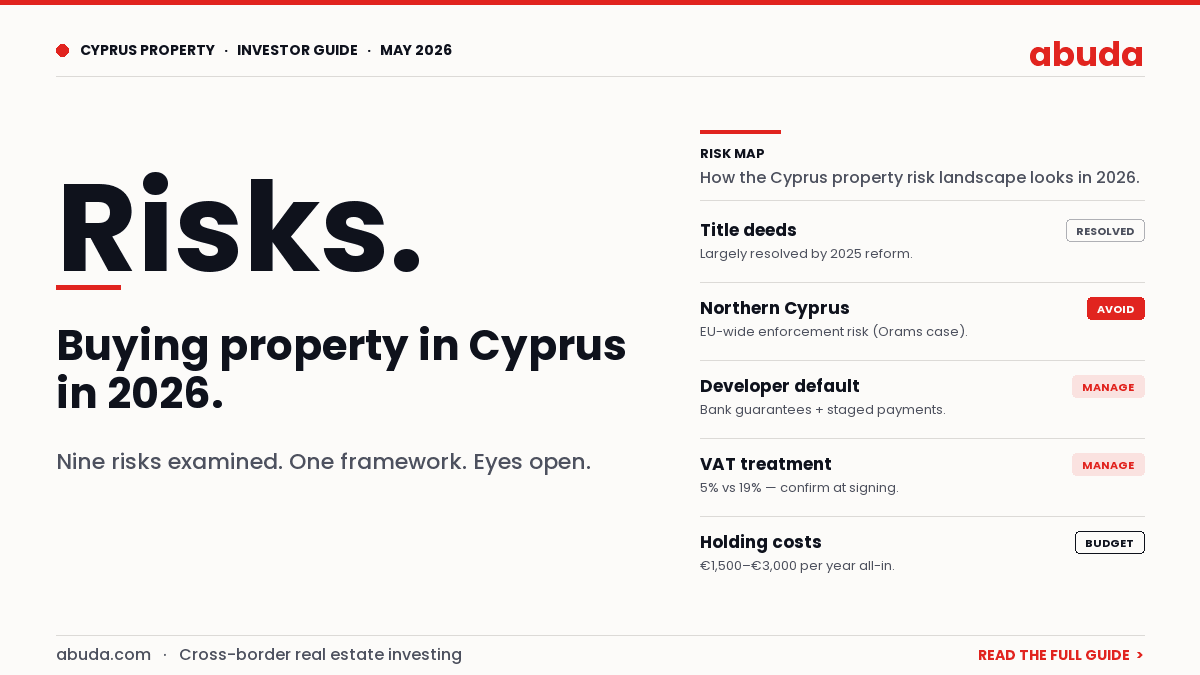

TL;DR — The Cyprus Property Risk Landscape in 2026

For the time-pressed:

Title deed risk — historically the single biggest concern, has been substantially de-risked by the 2025 Trapped Buyers Law passed by the House of Representatives on 26 June 2025. Always still verify the developer's track record on deed issuance.

Northern Cyprus risk — material and enforceable across the EU after the Apostolides v Orams judgment (ECJ, 2009). Do not buy in the Turkish-occupied area; only purchase in the Republic of Cyprus (the south).

Holding cost risk — communal fees of €50-€200/month and electricity costs (driven by heavy A/C use) are real ongoing expenses; budget for them upfront.

Off-plan / developer default risk — manageable through bank guarantees, staged payments, and choosing developers with a Certificate of Final Approval history.

VAT complexity — 5% on a primary residence (under specific criteria) vs. 19% on second homes and investment property — get this right at the purchase stage.

Liquidity, regulatory, and succession risks — present but not unique to Cyprus; addressable with proper planning.

Now the detail.

1. The Title Deeds Problem — Historically #1, Substantially Resolved in 2025

For two decades, the "title deeds problem" was the single most-cited reason to be cautious about buying property in Cyprus. Buyers who had paid the full purchase price found themselves unable to receive the actual title deed to their property, often because the developer or land seller had pre-existing mortgages or other encumbrances on the underlying plot. By the time the Supreme Court of Cyprus invalidated core provisions of the 2015 framework in June 2024, approximately 9,500 buyers were classified as "trapped".

What changed: the 2025 Trapped Buyers Law

On 26 June 2025, the House of Representatives passed a new constitutionally-compliant amendment to the Immovable Property (Transfer and Mortgage) Law. The headline provisions are material:

Court-ordered consent: Where lenders or other charge-holders refuse to consent to the title transfer despite the buyer having paid in full, a buyer can now petition the court for a substitute order. This breaks the deadlock that defined the old system.

Two-year, eight-month deadline: Title deeds must be issued within that window from the law's enactment, creating a clear path to resolution rather than indefinite delay.

Eligibility cut-offs: The law covers buyers who lodged sale contracts with the Land Registry by 31 December 2014, or with District Courts by 31 December 2024 — meaning anyone signing a clean contract in 2026 with a reputable developer is operating in a fundamentally different legal environment.

What this means for a 2026 buyer

The historical title-deed risk has been substantially de-risked. But "substantially" is not "completely". Three practical guardrails still apply:

Only buy from developers with a clean deed-issuance track record. Ask directly: "Show me the last 10 units you delivered and the date the title deed was issued to each buyer."

Insist on a Certificate of Final Approval (the legal certification that the building has been constructed in accordance with the planning permission and is fit for transfer of separate title).

Verify the underlying land is free of prior encumbrances before you sign. Your independent Cyprus lawyer should do a full Land Registry search and report on this before you wire any funds.

The infrastructure to do this properly exists. The diligence is straightforward. The historical problem was buyers skipping these steps.

2. Northern Cyprus: The One Risk You Cannot Mitigate

This is the most clear-cut "do not do this" in Cyprus property. Buying property in the Turkish-occupied northern part of the island ("TRNC") is fundamentally different from buying in the Republic of Cyprus in the south, and the legal risk is permanent, asset-wide, and enforceable across the European Union.

The Apostolides v Orams case

In 2002, a British couple, David and Linda Orams, purchased land in northern Cyprus from a seller registered under TRNC law, and built a villa on it. The original Greek Cypriot owner, Meletios Apostolides — who had been displaced when the island was divided in 1974 — sued in the Nicosia District Court, which is a Republic of Cyprus court.

In November 2004, the Nicosia court ordered the Orams to demolish the villa, the swimming pool, and the fencing, hand the land back to Apostolides, and pay damages. The Orams appealed.

The case escalated all the way to the European Court of Justice. In April 2009, the ECJ ruled that the EU regulation on enforcement of judgments did apply — meaning that UK courts (and the courts of every other EU member state) were legally obliged to enforce the Nicosia judgment. The Orams faced the prospect of the Nicosia ruling being enforced against their family home in Sussex.

Why this is structurally different from any other Cyprus property risk

Most property risks are about the specific asset you buy. Northern Cyprus risk is about everything else you own in the EU. A purchase that turns out to be on disputed land creates a judgment that can be enforced against any of your other assets in the United Kingdom, Germany, France, or any EU member state.

Both the British High Commission in Cyprus and the UK Foreign and Commonwealth Office have issued explicit warnings about purchases in the north. So have most major property law firms operating on the island.

The practical rule

If you are buying property in Cyprus for any purpose — residence, investment, retirement, holiday home — buy in the Republic of Cyprus (the south). Limassol, Larnaca, Pafos, Nicosia (the southern, internationally-recognized part), Ayia Napa, Polis. The legal certainty in the south is on par with any other EU member state. The legal certainty in the north is unresolved and may remain so for decades.

This is the one risk in Cyprus property that you cannot price or hedge. The only sound mitigation is to avoid the exposure entirely.

3. Maintenance and Holding Costs You Won't See on the Listing

The advertised price is what you pay to acquire the property. The numbers below are what you pay every month to own it. They're not large, but they need to be in your financial model.

Communal fees

Apartment buildings and complexes in Cyprus charge communal fees that cover the upkeep of shared spaces — lobbies, lifts, pool maintenance, gardens, gym, security, building insurance, common-area cleaning. Typical monthly ranges:

€50-€80 for older buildings without significant amenities.

€80-€150 for modern mid-range developments with a pool and basic security.

€150-€200+ for high-end developments with full amenity packages — gym, concierge, beach club access, EV charging, etc.

The single most important variable is the amenity profile of the development. A property in a Limassol marina-front complex with concierge service and a hotel-style spa will sit at the top of this range; an unbranded mid-rise in inland Larnaca will sit at the bottom.

Electricity

Cyprus electricity is expensive by EU standards, and air-conditioning use is heavy from May through October. For an investor leasing an apartment to a year-round tenant, the tenant typically covers this directly, so it's not a landlord cost. But for short-term rentals (Airbnb-style), the host typically absorbs utilities, and a peak-summer month can run €200-€350 on a two-bedroom unit running A/C across multiple rooms.

Other recurring costs to budget

Building insurance: usually included in communal fees but sometimes paid separately on freehold villas.

Property management: 10-20% of gross rent for full-service management (tenant sourcing, rent collection, maintenance dispatch, periodic inspection). Material if you're a non-resident landlord.

Sewerage tax: a small municipal charge, typically €100-€300/year depending on the property's rateable value.

Refuse collection: similar magnitude.

A reasonable annual holding-cost assumption on a mid-market two-bedroom Limassol apartment is roughly €1,500-€3,000 per year all-in, before management fees. This is small relative to gross rent of €15,000-€20,000+ on the same unit, but it should be in your spreadsheet from day one.

4. Developer Default and Off-Plan Risk

When you buy off-plan, you're paying a developer to deliver a future asset. If the developer goes insolvent before delivery, you become an unsecured creditor in their liquidation. This is a real risk in any market — Cyprus is not unique — but the mitigations are well-established:

Bank guarantees: a reputable developer will provide a bank-issued guarantee that ring-fences your deposits until delivery milestones. Insist on this.

Staged payments tied to construction progress: avoid contracts that front-load payments. A typical schedule is 30% on reservation, 30% on foundations, 30% on shell completion, 10% on delivery.

Escrow arrangements for the final tranche held by your lawyer rather than passed directly to the developer.

Developer reputation and balance sheet: ask for the developer's last three completed projects, the timelines, the delivery dates, and customer references. The construction industry in Cyprus is consolidated enough that bad actors are well-known.

The 2025 Trapped Buyers Law also makes it materially harder for a developer to walk away from a building project with buyers' money — the legal infrastructure has tightened around developer obligations.

5. VAT — Get It Right at Purchase Stage

VAT on Cyprus property is one of the easiest places to overpay simply by misunderstanding the rules:

5% VAT applies to the first 130 sqm of a primary residence purchase from a developer, subject to the buyer using the property as their main residence and not owning another primary residence in Cyprus. There are anti-abuse rules — you must actually live in it for a defined period.

19% VAT applies to second homes, investment property, and any portion of a primary residence beyond the 130 sqm threshold or other size/value caps.

For an investor buying for rental, 19% is the default. Some structures — for example, holding through a Cyprus company, or buying a resale property where the VAT cycle has already closed — can change the effective VAT burden, but these need to be evaluated case by case with a Cyprus tax advisor.

The single most expensive mistake here is structuring a purchase as a "primary residence" to qualify for 5% VAT when you have no intention of actually living in the property. The Cyprus Tax Department audits this, and being caught means paying back the differential plus penalties.

6. Liquidity and Resale Risk

Cyprus property is liquid where there's depth — central Limassol, the coastal strip, the marina, and prime Pafos resort areas can be sold within 3-6 months in a normal market. Off the coastal strip, in less-developed inland neighbourhoods, or in oversupplied micro-markets, resale timelines can extend to 12-24 months.

Three practical points:

Buy where the resale market is deep. This is the single biggest determinant of liquidity, and it's not the same as where the highest yield is.

Capital Gains Tax of 20% applies on resale profits, subject to the €30,000 general exemption raised by the 2026 tax reform. Hold periods matter — there's no short-term penalty, but factor CGT into your net return projection.

Marketing infrastructure matters. Properties sold through established agents and digital platforms move faster than those listed only locally. Plan your exit before you enter.

7. Regulatory and Political Risk

Cyprus is an EU member state with a stable rule of law and broadly predictable regulatory framework. That said, two specific areas have changed recently and may continue to change:

Tax framework: the 2026 tax reform abolished stamp duty and the Special Defence Contribution on rental income, raised CGT exemptions, and tightened the "property-rich company" rules (threshold dropped from 50% to 20%). The direction of travel has been investor-favourable, but tax law changes, and structures that work today may need adjustment later.

Short-term rental regulation: Cyprus has introduced licensing requirements for short-term tourist rentals. Compliance is straightforward but mandatory. Also, from July 2026, all rent payments over €500 must be made electronically — a transparency measure rather than a yield headwind, but a compliance step landlords need to be ready for.

Neither of these is unusual or onerous by EU standards, but neither is static. Build a relationship with a Cyprus tax advisor and revisit your structure annually.

8. Building Quality and Climate Risk

Cyprus sits on the Anatolian fault system and is subject to seismic activity. Construction standards have tightened over the last 15 years, and modern developments built to current code are engineered for the relevant seismic zone. Older buildings — particularly 1970s and 80s stock — should be evaluated for retrofit need before purchase. A structural survey is non-negotiable on any property older than 20 years.

Climate is the other under-priced exposure. Mediterranean heat and humidity stress materials. Coastal salt air corrodes metal fixtures, balconies, and air-conditioning units. Energy-efficiency regulations are tightening across the EU, and older Cyprus stock will face capex pressure to upgrade insulation, glazing, and HVAC. Modern A-rated builds avoid this; older stock should be priced accounting for it.

9. Succession and Estate Planning

Cyprus has forced heirship rules under its succession law — a portion of an estate must pass to specified close relatives, regardless of what the will says. For an international investor, this can produce outcomes that don't align with home-country estate plans.

Mitigations are well-established and routine: holding through a Cyprus company structure, drafting a will under Cyprus law that addresses the forced heirship portion explicitly, or relying on the EU Succession Regulation (No 650/2012) which can allow nationals of EU member states to elect the law of their nationality for their estate. This needs to be coordinated between your home-country estate lawyer and a Cyprus lawyer — not done in isolation.

A 10-Point Pre-Purchase Checklist

A summary of the practical mitigations across all the risks above:

Engage an independent Cyprus lawyer — not the one introduced by the developer.

Run a Land Registry search for prior encumbrances on the underlying plot.

Verify the developer's deed-issuance track record on their last 10 completed projects.

Insist on a Certificate of Final Approval for the building.

Buy only in the Republic of Cyprus — never in the north.

Use bank guarantees and staged payments for off-plan purchases.

Confirm your VAT treatment with a Cyprus tax advisor before signing.

Budget annual holding costs at €1,500-€3,000 for a mid-market apartment.

Get a structural survey on any property older than 20 years.

Address succession planning before the purchase, not after.

None of these are extraordinary. All of them are skipped routinely by buyers who later regret it.

Frequently Asked Questions

What is the title deeds problem in Cyprus?

The title deeds problem refers to a historical situation where Cyprus property buyers paid the full purchase price but were unable to receive the actual title deed to their property, usually because of pre-existing mortgages or other encumbrances on the underlying land. Approximately 9,500 buyers were classified as "trapped" before the 2025 legal reform. The 2025 Trapped Buyers Law, passed by the Cyprus House of Representatives on 26 June 2025, provides a constitutionally compliant resolution path with a 2-year-8-month deadline for deed issuance.

Is it safe to buy property in Northern Cyprus?

No — buying property in the Turkish-occupied northern part of Cyprus carries material legal risk. The 2009 European Court of Justice ruling in Apostolides v Orams confirmed that judgments by Republic of Cyprus courts ordering the return of disputed northern land are enforceable across the EU, including against your other assets. Both the UK Foreign Office and the British High Commission in Cyprus have issued warnings about purchases in the north. Only the Republic of Cyprus (the south) provides legal certainty.

What are typical maintenance costs for an apartment in Cyprus?

Communal fees on a Cyprus apartment typically run €50-€200 per month, depending on the building's amenity profile (pool, gym, concierge, etc.). Electricity is expensive due to heavy summer air-conditioning use — peak months can run €200-€350 on a two-bedroom unit. Total annual holding costs on a mid-market two-bedroom apartment, excluding rent management fees, typically land in the €1,500-€3,000 range.

What VAT rate applies to property in Cyprus?

5% VAT applies to the first 130 sqm of a primary residence purchased from a developer, subject to use as the buyer's main home. 19% VAT is the default for investment property, second homes, and any portion above the size/value thresholds. Resale properties where the VAT cycle has closed may not attract VAT at all. Get the VAT treatment confirmed by a Cyprus tax advisor before signing — mistakes here are expensive and audited.

How do I protect myself when buying off-plan property in Cyprus?

Use bank guarantees that ring-fence your deposits until delivery milestones, structure staged payments tied to construction progress (typical: 30% on reservation, 30% on foundations, 30% on shell completion, 10% on delivery), keep the final tranche in lawyer-held escrow, and verify the developer's last three completed projects. The 2025 Trapped Buyers Law has also tightened the broader legal framework around developer obligations.

Can foreigners inherit Cyprus property without issues?

Cyprus has forced heirship rules under its succession law that may not align with the estate plan of a non-Cyprus buyer. Mitigations include holding through a Cyprus company, drafting a Cyprus-law will that addresses the issue explicitly, or relying on the EU Succession Regulation 650/2012, which lets EU nationals elect the law of their nationality to govern their estate. Coordinate with both a Cyprus lawyer and your home-country estate lawyer.

What is the most underestimated risk for foreign buyers in Cyprus?

Building quality and energy-efficiency capex risk on older stock. Buyers often focus on the historical title deeds issue (now largely resolved) and overlook the very real capex pressure that tightening EU energy regulations will place on pre-2010 buildings over the next decade. Buying A-rated new builds avoids this; buying older stock at a discount that doesn't account for retrofit costs underprices the risk.

What's Next

If you'd like to see specific projects in the markets where the risk landscape is best understood — Limassol, Larnaca, and Pafos with developers who have a clean title-deed record — browse the curated Cyprus inventory on Abuda or contact the Abuda sourcing team at hello@abuda.com.

For the broader Cyprus vs. Berlin comparison framework, see our Q1 2026 Global Investment Matrix.

For the on-the-ground developer landscape we've personally met with, see our REALTYon Cyprus 2026 recap.

This article is informational and does not constitute legal, tax, or investment advice. Property markets and tax regulations change. Always work with a qualified Cyprus lawyer and tax advisor before making a purchase decision.