Limassol vs. Larnaca vs. Berlin: Where to Invest in European Real Estate in 2026

Limassol vs. Larnaca vs. Berlin: Where to Invest in European Real Estate in 2026

Published 12 May 2026 by Kefah Abu Ghosh, Founder of Abuda — built on Abuda's Global Investment Matrix.

TL;DR — The Short Answer

If you're choosing between Limassol, Larnaca, and Berlin for an investment property in 2026, the trade-off is simple but real:

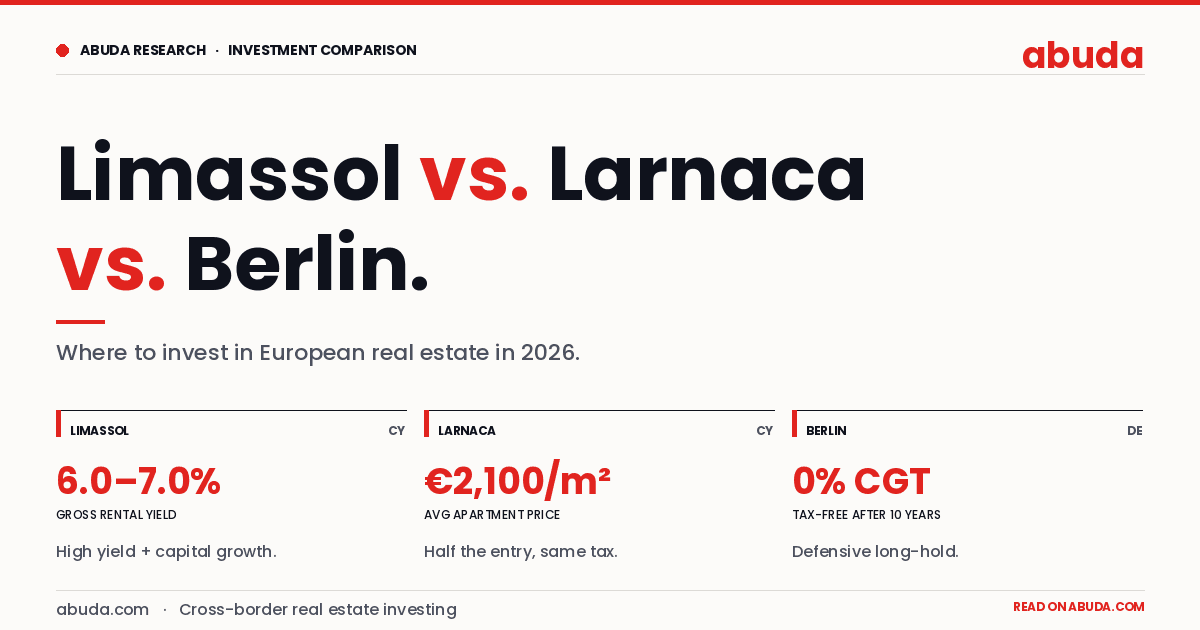

Limassol delivers the highest gross rental yields (6.0%–7.0%) and the strongest capital growth momentum (7.0%–10.4% YoY), backed by a 2026 tax reform that abolishes stamp duty and the SDC on rental income. Best for yield-seeking investors and growth capital.

Larnaca is the value play. Apartment prices average €2,100–€2,400 per sqm (well below Limassol), gross yields of 5.4%–7.4%, and price growth that quietly outpaced Limassol in 2025. Best for investors who want Cyprus exposure with a lower entry ticket.

Berlin is the defensive choice. Yields are lower (2.5%–3.5%) and acquisition costs are higher (10%–12%), but Germany's "10-year rule" delivers 0% capital gains tax after a decade of ownership. Best for patient capital and tax-optimized long holds.

This article unpacks each of those positions with the data, the tax detail, the regulatory context, and a five-year ROI projection for each market.

The Three Markets at a Glance (Q4 2024 Baseline, 2026 Regulatory Update)

Metric | Limassol | Larnaca | Berlin |

|---|---|---|---|

Gross rental yield | 6.0% – 7.0% | 5.4% – 7.4% | 2.5% – 3.5% |

Average rent per sqm | ~€32 | ~€18 – €20 | €18 – €24 (prime) |

Avg. apartment price per sqm | ~€4,500 – €5,500 | ~€2,100 – €2,400 | ~€5,500 – €7,000 (prime) |

Capital growth (YoY 2024–25) | 7.0% – 10.4% | ~6% | 3.8% – 9.0% |

Occupancy rates | 90% – 98% | 90% – 95% | 98% – 99%+ |

Total acquisition costs | ~1.9% (post-2026 reform) | ~1.9% (post-2026 reform) | 10% – 12% |

Annual property tax | 0% | 0% | Grundsteuer (~0.2%) |

Capital gains tax | 20% flat | 20% flat | 0% after 10 years |

Market maturity | Emerging business hub | Emerging value market | Established institutional core |

These figures form Abuda's Q4 2024 Global Investment Matrix and are normalized for total acquisition costs and the 2026 Cyprus tax reform.

Limassol: The High-Yield, High-Growth Mediterranean Hub

Limassol has spent the last five years transforming from a coastal resort town into the headquarters city of choice for international shipping, fintech, and crypto operators across the eastern Mediterranean. Over 80 nationalities are now active in the city, and that demographic shift is the engine behind both the rent and price growth that puts Limassol at the top of European yield rankings.

Yield and growth in Limassol

In Q4 2024, gross rental yields in Limassol sat in the 6.0% to 7.0% range, with average rents of approximately €32 per sqm per month — comfortably ahead of Berlin's prime rents and roughly 1.5x the rents in Larnaca. Capital growth was even more striking: 7.0% to 10.4% year-on-year, driven by genuine end-user demand rather than speculative capital.

A notable Q4 2024 dynamic: new energy-efficient apartments are appreciating faster than houses. This matters for an investor optimizing both for capital growth and for compliance with EU energy-performance regulations, where higher-grade EPC ratings are increasingly priced into both rental and resale values.

The 2026 Cyprus tax reform — and what it means for Limassol investors

The 2026 Cyprus tax reform, effective 1 January 2026, materially improves the after-tax returns on Limassol property:

Stamp duty is abolished for property contracts. This removes the previous 0.15%–0.20% upfront cost on the purchase contract.

Special Defence Contribution (SDC) on rental income is abolished for tax residents — this effectively lifts net yields by approximately 2.25 percentage points.

A 50% discount on Transfer Fees continues to apply to resale properties not subject to VAT.

The lifetime CGT exemption on the primary residence is raised to €150,000 (from €85,430), and the general exemption to €30,000.

For an investor buying a €500,000 apartment in Limassol's coastal strip and renting it at €32 per sqm, the post-reform net yield lands between 4.5% and 5.0% — and the 2026 acquisition cost is essentially just notary and legal fees, in the ~1.9% range.

Risks to know

Limassol's rental market is not rent-capped the way Berlin's is, but from July 2026, all rent over €500 must be paid electronically for transparency purposes — a minor compliance change rather than a regulatory headwind. Supply is being added quickly, which means the next 24 months will test whether Limassol's growth rate can sustain the 7%+ trajectory. Our base case at Abuda is that yields stay strong but capital growth moderates toward the lower end of the 7%–10% range.

Larnaca: The Underpriced Cyprus Alternative

If Limassol is the institutional play, Larnaca is where the value-conscious investor should be looking in 2026. This is also the market the headline indices have been quietly telling us about: in 2025, apartment prices in Larnaca rose ~6% versus Limassol's ~3%, with the district benefiting from infrastructure investment, the airport-adjacent logistics, and a growing population of remote workers and digital nomads.

Yield and price in Larnaca

Larnaca's gross rental yields range from 5.4% to 7.4%, with city-centre apartments typically clearing 6.76% to 7.41% — actually above the equivalent yield bracket in central Limassol on a per-square-metre basis, because entry prices are dramatically lower.

Average apartment prices in Larnaca sit at €2,100 – €2,400 per sqm, compared to roughly €4,500 – €5,500 per sqm in Limassol's investment-grade coastal areas. That means a comparable 80 sqm two-bedroom apartment costs roughly €170,000 – €190,000 in Larnaca versus €360,000 – €440,000 in Limassol. For investors deploying €200k–€400k of equity, Larnaca lets you build a two- or three-unit portfolio for the price of a single Limassol unit.

Average rents in Larnaca currently sit at approximately €575 for one-bedroom, €738 for two-bedroom, and €900 for three-bedroom apartments. These are baseline numbers — premium new-build supply in the marina and seafront areas commands meaningfully higher rents.

Why Larnaca, why now

Three structural drivers we're tracking at Abuda:

The marina redevelopment and airport-adjacent infrastructure are pulling forward what was previously seen as a sleepy secondary market. Larnaca's location — 45 minutes to Limassol, 50 minutes to Nicosia, walking distance to the airport — is increasingly being priced in.

The remote-work population has been growing year-on-year, driven by Cyprus's digital nomad visa and the relatively low cost of living vs. Limassol.

Pre-sale and off-plan supply is opening up — at REALTYon Cyprus 2026, we saw new product from developers including Infinity Properties and MZ Residence specifically targeting investor buyers in Larnaca's growing residential corridors.

The same 2026 Cyprus tax reform benefits — abolished stamp duty, abolished SDC on rental income, raised CGT exemptions — apply equally to Larnaca property. So Larnaca offers Limassol's tax treatment at roughly half the entry price.

Berlin: Defensive Yield, Tax-Free Exit

Berlin is the structural opposite of Limassol. Lower yield, higher entry costs, much higher regulatory friction — but a tax exit that no Cyprus market can match, and a chronic supply-shortage story that has underwritten capital values through every European cycle since 2010.

Yield and growth in Berlin

Gross rental yields in Berlin sit in the 2.5% to 3.5% range in Q4 2024 — significantly below Cyprus, and lower than they were five years ago because price growth has outpaced rent growth. Average prime rents are €18 – €24 per sqm, with the lower 10% rent category seeing increases of 13.1% — the clearest signal in the data that affordability is breaking down and that political pressure on rents will continue.

Year-on-year capital growth was 3.8% to 9.0%, depending on segment. Established prime districts grew at the lower end; emerging-to-prime transitional neighbourhoods (Wedding, parts of Lichtenberg, the eastern arc into Pankow) at the upper end.

Acquisition costs — the real Berlin headwind

This is where Berlin loses to Cyprus by a wide margin. Total acquisition costs in Berlin run 10% to 12% of purchase price, comprising:

6% Property Transfer Tax (Grunderwerbsteuer) — paid on completion.

Notary fees: approximately 1.5%.

Agent commission: approximately 3.57% including VAT (now legally split between buyer and seller).

By comparison, post-2026 Cyprus acquisition costs are essentially just legal and registration — roughly 1.9% of purchase price. This 8-10 percentage point cost differential takes years of yield to recover, which is why Berlin works for long-hold patient capital but is structurally inefficient for short-to-medium-hold strategies.

The 10-year rule — Berlin's hidden weapon

Germany's tax code includes one of the most investor-friendly capital gains provisions in Europe: if a private individual holds residential property for at least 10 years, capital gains on sale are completely tax-free.

For an investor buying a €600,000 apartment in Berlin in 2026, holding through 2036, and selling at, say, €820,000, the €220,000 gain is taxed at 0%. In Cyprus, the same gain (after applying the €30,000 general exemption) would attract 20% CGT — approximately €38,000 of tax. The longer the hold, the more this differential compounds.

This is the lever that makes Berlin work despite the lower yield and higher entry friction. It is not a yield play. It is a tax-efficient compounding play for patient capital.

Regulatory: Mietpreisbremse and rent control

Berlin operates under one of Europe's strictest rent regulation regimes. The Mietpreisbremse (rent cap) has been extended until 2029, which limits re-letting rents to no more than 10% above the local comparative rent index (Mietspiegel). For investors, this means:

Rent growth on existing tenancies is capped.

Re-letting rents are constrained by the index.

The biggest yield-uplift opportunity is buying vacant units (priced higher but unlocked from rent cap) and energy-efficiency-driven rent increases tied to capex (modernization surcharges).

The supply story remains structurally favourable — Berlin is short tens of thousands of units per year against demand — which is why prices have continued to rise despite the rent cap. But yield expansion is essentially capped.

Tax and Cost Comparison: What You Actually Pay

Cost or tax | Limassol & Larnaca (2026) | Berlin (2026) |

|---|---|---|

Stamp Duty | Abolished from 1 Jan 2026 | N/A |

Transfer Tax | 50% discount on resale (no VAT) | 6% (Grunderwerbsteuer) |

Notary fees | ~0.5% – 1% | ~1.5% |

Agent commission (buyer side) | typically nil for buyer | ~3.57% (incl. VAT) |

Total acquisition cost | ~1.9% | 10% – 12% |

Annual property tax | 0% | Grundsteuer (~0.2%) |

SDC on rental income | Abolished 2026 | N/A |

Effective net yield uplift from reform | +~2.25% | N/A |

Capital gains tax on sale | 20% flat (with €30k+ exemptions) | 0% after 10 years (private) |

The single most consequential number on this table is the 2.25 percentage point net yield uplift delivered by the SDC abolition in Cyprus. On a €500,000 Limassol apartment generating 6.0% gross yield, the post-reform net yield uplift is worth roughly €11,250 per year in additional after-tax income versus the pre-2026 regime.

5-Year ROI Scenarios

Numbers below are illustrative projections, not guarantees, and assume a 5-year hold with rents and capital values growing in line with each market's base-case trajectory.

Scenario | Limassol (optimistic) | Larnaca (base) | Berlin (conservative) |

|---|---|---|---|

Annual capital appreciation | 5.0% – 7.0% | 4.0% – 6.0% | 2.0% – 3.0% |

Net rental yield (post-reform) | 4.5% – 5.0% | 4.5% – 5.5% | 1.8% – 2.4% |

Total annual return | ~10% – 12% | ~9% – 11% | ~4% – 5% |

Holding-period tax | 0% (no annual property tax) | 0% (no annual property tax) | ~0.2% Grundsteuer |

Exit tax (5-year hold) | 20% CGT on profit | 20% CGT on profit | Subject to CGT (under 10-year rule) |

Exit tax (10-year+ hold) | 20% CGT on profit | 20% CGT on profit | 0% — tax-free |

The headline takeaway: on a 5-year hold, Limassol and Larnaca dominate Berlin on total return. On a 10-year+ hold, Berlin's tax-free capital gains provision narrows or closes the gap, depending on how much of the total return is capital growth vs. yield.

Which Market Fits Which Investor?

Choose Limassol if:

You want the highest immediate cash flow and you're comfortable deploying €400k+ per unit.

You're targeting yield-driven returns with capital growth as a tailwind.

You want exposure to the international "headquartering" demand profile (shipping, fintech, crypto).

You're a non-resident investor and you value Cyprus's transparent, English-language transaction process.

Choose Larnaca if:

You're deploying €150k–€400k per unit and want to build a portfolio rather than a single asset.

You believe Larnaca's recent ~6% growth is the start of a multi-year catch-up trade vs. Limassol.

You're optimizing for risk-adjusted yield with lower absolute price exposure.

You want airport-adjacent or marina-adjacent inventory for short-term rental strategies.

Choose Berlin if:

You have patient capital (10+ year horizon) and are optimizing for after-tax compounding.

You want institutional-grade asset quality, liquidity, and exit certainty.

You're willing to accept lower yield and higher acquisition costs in exchange for the 10-year CGT exemption.

You want defensive exposure to a market backed by structural housing undersupply.

The strongest portfolio combination

Many of the cross-border investors we work with at Abuda combine these markets — Limassol or Larnaca for yield and short-to-medium-term capital growth, Berlin for tax-efficient long-hold compounding. The two strategies are complementary rather than competing: one funds the other.

Frequently Asked Questions

What is the rental yield on an apartment in Limassol in 2026?

Gross rental yields in Limassol range from 6.0% to 7.0% in Q4 2024 baseline data. After the 2026 abolition of the Special Defence Contribution on rental income, net yields for tax-resident investors land in the 4.5% to 5.0% range — among the highest in the European Union.

Is Larnaca a good place to buy investment property in 2026?

Yes. Larnaca offers gross rental yields of 5.4% to 7.4%, average apartment prices of €2,100 – €2,400 per sqm (about half the Limassol equivalent), and capital growth that outpaced Limassol's in 2025. For investors deploying €150k–€400k per unit, Larnaca is the most attractive risk-adjusted Cyprus market in 2026.

How much does it cost to buy property in Berlin?

Total acquisition costs in Berlin run 10% to 12% of purchase price, including 6% Property Transfer Tax (Grunderwerbsteuer), approximately 1.5% notary fees, and around 3.57% agent commission (including VAT). This is the highest acquisition-cost profile of any major European capital and is the structural reason Berlin works only for long-hold strategies.

Can foreigners buy property in Cyprus?

Yes. EU citizens face essentially no restrictions when buying property in Cyprus. Non-EU buyers can also purchase, subject to Council of Ministers approval, which is a routine administrative process for residential property up to two units.

What was abolished in the 2026 Cyprus tax reform?

The 2026 Cyprus tax reform, effective 1 January 2026, abolished stamp duty on property contracts (previously 0.15% – 0.20%) and the Special Defence Contribution on rental income for tax residents. It also raised the lifetime capital gains tax exemption on a primary residence to €150,000 (from €85,430) and the general CGT exemption to €30,000.

Does Berlin have rent controls?

Yes. The Mietpreisbremse (rent cap) has been extended through 2029, limiting re-letting rents to no more than 10% above the local comparative rent index. Rent growth on existing tenancies is also constrained. Investors targeting yield uplift in Berlin typically buy vacant units, where the rent cap does not bind initial pricing, or pursue energy-efficiency modernization which permits regulated rent increases.

What is pre-pre-sale property?

Pre-pre-sale is the stage before a developer publishes pricing and opens public reservations. Inventory is allocated through trusted partners and platforms — usually with the lowest entry pricing of the entire development cycle and the broadest unit selection. Abuda specializes in giving cross-border investors access to pre-pre-sale inventory across Limassol, Larnaca, and Berlin.

Which is better for foreign investors — Cyprus or Germany?

It depends on the holding period. For 5-year holds, Cyprus (Limassol or Larnaca) wins decisively on total return — higher yield, lower acquisition cost, no annual property tax, and growth that outpaces Berlin. For 10-year+ holds, Berlin's tax-free capital gains provision under the German "10-year rule" can close or reverse the gap, particularly if capital growth dominates the total return profile. A blended portfolio captures the best of both.

What's Next

This article is built on Abuda's Q4 2024 Global Investment Matrix. The matrix itself — including the underlying data, normalized fee assumptions, and full methodology — is available to verified Abuda investors. If you're considering deploying capital into Limassol, Larnaca, or Berlin in 2026, the next step is to look at specific developments and unit-level data:

Browse available investment apartments on abuda.com → curated pre-pre-sale and off-plan inventory across all three markets.

Speak to our sourcing team → email k@abuda.com for direct access to projects not yet listed publicly.

Sign up for the Abuda investor list to be notified when new Limassol, Larnaca, and Berlin inventory comes onto the platform.